Buy a house or not? Refinance your mortgage or not? Millions of American families are facing these questions right now. Right now, thanks in large part to the Federal Reserve, mortgage rates are at all-time lows AND will likely stay there for a while (or even go lower). Although they don’t directly control mortgage rates, the Federal Reserve Board does indirectly influence mortgage rates. The Federal Reserve has shown that they are unlikely to raise short term interest rates (which they do control and which are currently at 0.00%-0.25%), until late 2022, at the earliest (look at the ‘dot plot’ on page 3).

What to do about the ‘hot’ housing market?

Even though the housing market is very ‘hot’ right now, there is a possibility that the housing market will cool if we don’t have a strong economic recovery coming out of the COVID-19 recession. If jobs don’t come back, unemployment will stay high and fewer people will be able to buy a house, and unfortunately, a slow recovery will likely lead to an increase in foreclosures, which could potentially put downward pressure on home prices. Another possibility is that the Baby Boomer generation starts to downsize in earnest as single-family home prices stay high or keep rising. This ‘Silver Tsunami’ could potentially put downward pressure on home prices if too many try to sell and buyer demand slows. If buyer demand dries up, due to any of the above situations, housing prices could stagnate or fall, making the housing market more favorable for buyers than sellers.

However, if the economy does come back strong, housing prices will likely keep increasing, but with the Federal Reserve keeping interest rates low, mortgage rates should not rise significantly from where they are now. If this happens, home prices will likely continue to rise with a stronger economy and low interest rates.

What about refinancing?

Refinancing is a different decision than purchasing. Right now, if you can significantly lower the interest rate on your mortgage, it is a great time to refinance your mortgage. With that being said, you can use this mortgage calculator to find out how much your potential new mortgage would cost and compare it with your current amortization tables to see how much you would save long term. (An amortization table shows the payments for the remainder of your current mortgage. It will break down each payment into principal and interest and should also give you a total at the end for total cost.) An additional factor is closing costs. If closing costs are too high, they could significantly reduce or even eliminate any savings from refinancing. Below are two examples for refinancing. Both examples assume a starting mortgage balance of $300,000, and the refinancing is based off the remaining mortgage balance. Example 1 shows refinancing 5 years into a 30-year mortgage. Example 2 shows refinancing 1 year into a 30-year mortgage. The main things to consider when refinancing would be the change in monthly payment, change in payoff date, and the total amount of mortgage payments.

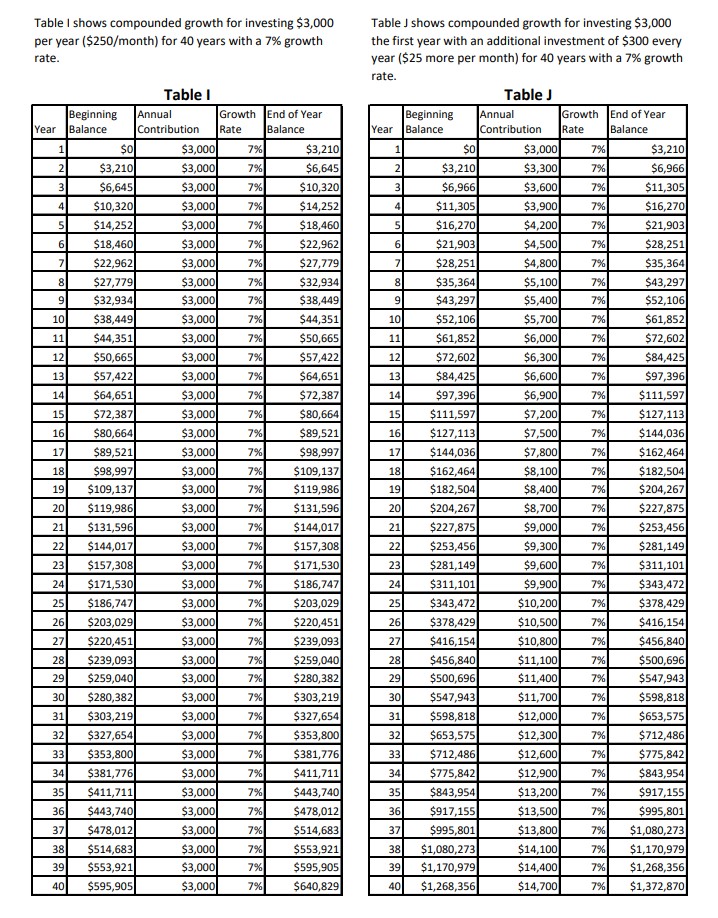

Based on these two examples, you will save more during the life of the mortgage if you refinance in the earlier years of the mortgage. The other aspect of this, especially for Example 1, is what will you do with the extra money from the reduced payment? If you invest that $250 per month ($3,000 per year), after 30 years of 7% growth, it grows to over $300,000. So if you are going to save and invest the savings from reduced mortgage payment, it is definitely worth it. However, if you’re just going to spend the difference, you might as well keep the higher mortgage payment in Example 1 because you will make 60 less mortgage payments. Refinancing shouldn’t be as simple as lowering your mortgage payment. Also, neither example factors in closing costs for refinancing.

{kind=link}

Conclusion

Right now, we are still in the midst of the COVID-19 pandemic. Cases are still rising in the U.S. and around the world. There is a lot of uncertainty now and in the future, and that uncertainty includes the future of the housing market. If refinancing will save you on your monthly payment and lower your total mortgage payoff, it is a great time to refinance, but as I discussed above, what you decide to do with the extra money every month should also be considered. If you’re looking to buy a house, mortgage rates are at historic lows and will probably stay there for a while. There is a chance that home prices keep rising, but there is also a chance that they stagnate or drop as well. Buying a house or refinancing a mortgage are major financial decisions, make sure you treat them that way.

Sign Up for the Weekly Off Ramp! And send in a topic you want to hear about on the Contact Us page. Follow me on Twitter ![]() Facebook

Facebook ![]() and Pinterest

and Pinterest ![]()