What would you do with an extra $100,000 during retirement? What could you do?

– Travel more

– Pay for grandchildren to go to college

– Buy a ‘Dream’ car

– Give more to charity

– Pay for a large family ‘destination’ vacation

– Make a house renovation you always wanted to make

What if it was $200,000 or $500,000? These may seem like incredibly large, unrealistic amounts of money, but they are possible for you to achieve. And this is just the extra amount you could have during retirement, only a small fraction of your nest egg, by making one change to your retirement savings.

Everyone wants to get to retirement, but not everyone plans well for it. Some people are saving very well for retirement and may already have a considerable nest egg. Some have a small nest egg growing in their retirement accounts, while others might be playing catch up. Time is arguably the most important factor when it comes to saving and investing for retirement. To see for yourself, take a look at the ‘Saving for Retirement: Now or Later?’ page on this blog. Be sure to click on the small tables to see a side by side comparison of how investing and saving early makes a very big difference over time. If you’re not yet saving for retirement, start sooner than later. If you are already saving, great job! Keep on saving or try to increase saving. Today, I’ll continue with the retirement theme of the last couple of weeks. The previous two retirement posts were about Roth IRAs and planning around a pension.

Questions to think about

For those of you who are saving for retirement and aggressively saving for retirement, you may end up with a significant size nest egg when you retire. If so, that’s great! However, I have a few questions for you to consider:

Have you considered the taxes you’ll pay on withdrawals from your retirement accounts?

What if you switched your traditional retirement contributions to Roth retirement contributions?

If you contribute to traditional retirement accounts and are eligible to contribute to Roth retirement accounts, is the income boost you get from contributing to traditional retirement accounts worth it?

How large will your required minimum distributions (RMD) be based on an average growth rate and continued contributions?

What will federal (and state) income tax rates be when you retire and which tax bracket will you fall in?

I know it is a bunch of questions to consider, but I’ll dig into the trade-off for saving in Roth retirement accounts versus traditional retirement accounts, especially when it comes to taxes on a large nest egg.

How large can your nest egg grow?

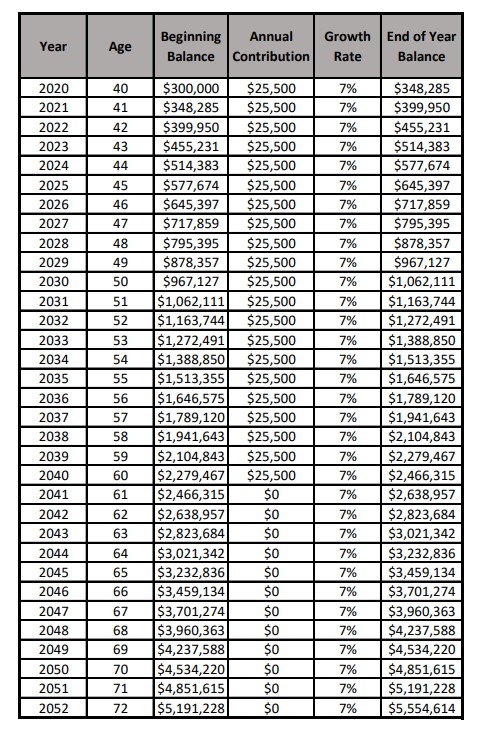

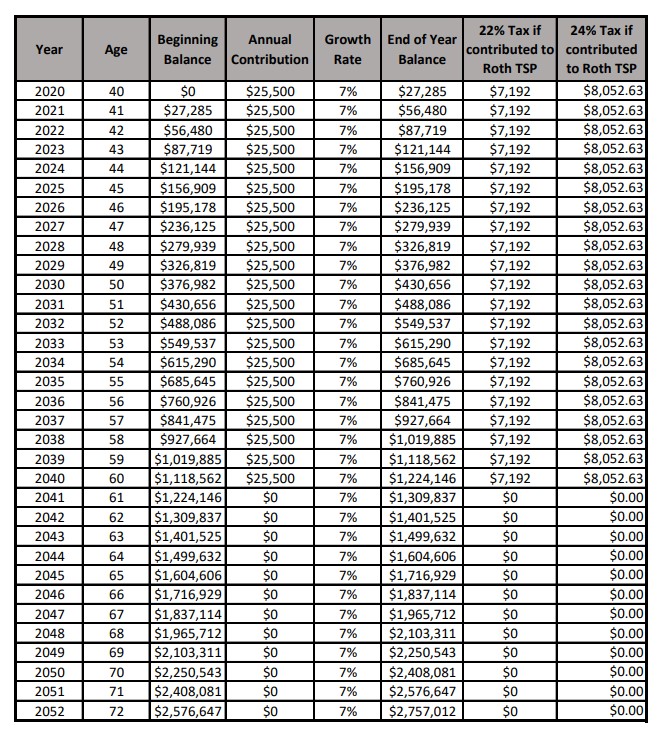

For this post, I wanted to use an individual or a family who is aggressively saving for retirement as an example. After doing a search for average retirement savings by age, I found this article to be the most informative for breaking down how much people (or a family) have saved within an age group. I also found that the average retirement savings for ages 35 to 44 is $100,000. For this example, we will assume a 40-year old person has saved three times the amount of the average, $300,000, and is continuing to contribute $25,500 per year ($19,500 maxing out a 401(k) or TSP and $6,000 for an IRA) until they are 60 years old. I’ll go over what happens for two situations: one person (or family) continues contributing to traditional retirement accounts and another person (or family) who changes their contributions to Roth retirement accounts. Both nest eggs will be the same size in total, but the difference will be taxes paid during retirement or during retirement contributions. Let’s see how the results turn out. The first table shows the results for the married couple filing jointly, and the second table shows the results for a single person.

As you can see, using Roth retirement accounts can save you a substantial amount in taxes down the road, especially if you are on track to have a large nest egg. For those married filing jointly, you’ll pay 30% less in taxes or $156,734. For single tax filers, you’ll pay over 36% less in taxes or $245,777. Remember, these estimates are only for the first 10 years of RMDs. Every year additional year will incur a larger tax bill for those only contributing to traditional retirement accounts. If you want to see the nest egg growth tables click on the links below:

Only Traditional Contributions (starting at $300,000) – $5,554,614 Nest Egg

{kind=link}

Change to Roth Contributions – $5,554,614 Nest Egg

– Traditional Account Growth (starting at $300,000) – $2,797,602 Nest Egg

– Roth Account Growth (starting at $0) – $2,757,012 Nest Egg

{kind=link}

{kind=link}

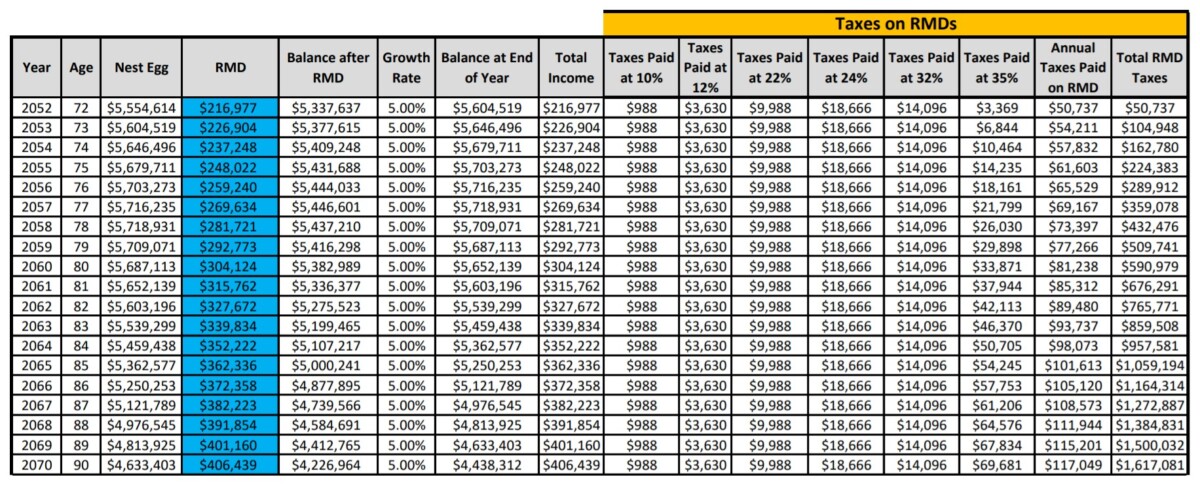

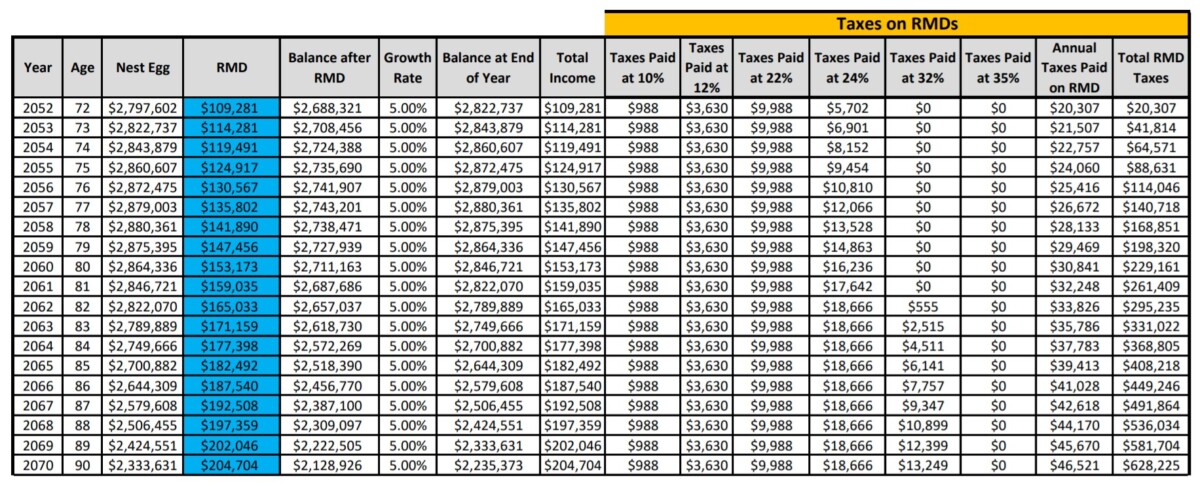

If you would like to see a breakdown of how the taxes would be paid during RMDs (after you turn 72 years old), below are links to two tables showing how taxes would be paid for each of the above nest eggs. Remember there are no taxes on withdrawals from Roth retirement accounts. The RMDs for the individual (or family) that has switched over to Roth retirement contributions will only have taxed RMDs on the nest egg that grew from their original $300,000 ($2,797,602 nest egg) and not the nest egg that grew from their Roth retirement contributions ($2,757,012 nest egg).

RMDs for Individual (or family) only making Traditional Retirement Contributions:

– Married Filing Jointly

– Single Tax Filers

{kind=link}

{kind=link}

RMDs for individual (or family) shifting to Roth Retirement Contributions – RMDs come from growth of only the original $300,000:

– Married Filing Jointly

– Single Tax Filers

{kind=link}

{kind=link}

If the Roth retirement accounts are consolidated into one Roth IRA during retirement, you will also be able to take money out of your Roth IRA when you want to, since there are no RMDs on Roth IRAs.

Wrapping Up

Although this post may seem unrealistic for many readers, it isn’t out of reach. If you don’t plan for retirement, you will have much less control over it. If you plan for retirement, it will be much more enjoyable (and probably more financially secure), but your planning needs to start now. Take a look at the ‘6 Steps of the Rat Race Off Ramp’ to get started. Reach out with any questions you may have.

I hope you can see the advantages that Roth retirement accounts can provide during retirement, especially regarding taxes. And the tax differences will be even larger if you will have a pension during retirement. Another consideration is income tax rates could be higher in the future.

If you’re interested in looking at your own numbers, I’m building a spreadsheet that will work as a calculator to help you do your own planning. If you’re interested in getting it, head over to the ‘Contact Us’ page or sign up for the weekly email. If you’re already signed up for the weekly email, you’ll get the spreadsheet calculator when it is ready to be sent out.

Sign Up for the Weekly Off Ramp! And send in a topic you want to hear about on the Contact Us page. Follow me on Twitter ![]() Facebook

Facebook ![]() and Pinterest

and Pinterest ![]()