Last week, I wrote about how Roth IRAs are the most powerful retirement accounts. If you’re in the military and saving in an IRA or TSP, or if you will get any pension during retirement (including social security), read this post carefully because I’m going to show why saving in a Roth IRA or Roth TSP will likely save you a lot in taxes over your lifetime and put more money in your pockets during retirement.

A few months ago, I wrote a post with estimated military retirement pay. For the examples in today’s post, I used the estimates for retiring in 2021, and I didn’t account for a cost of living allowances (COLA), which are increases in military retirement pay equal to any annual increase in social security pay. I also made calculations based on 2020 tax brackets for people who are married and filing jointly. I’ll go through one example thoroughly and provide tables for a handful of other examples. Military retirement pay and other pensions will be taxed as income for the rest of your life. Social security is taxed differently, but if you are going to get a military pension, you’ll likely incur the maximum possible taxes on your social security income. With that, let’s get started.

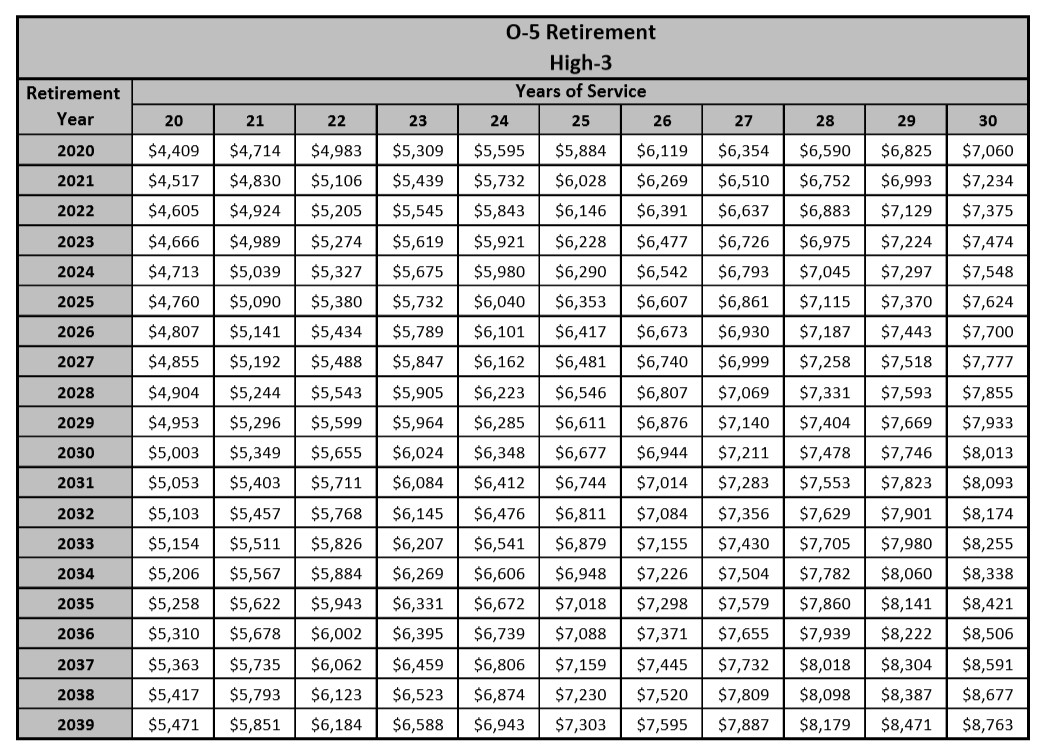

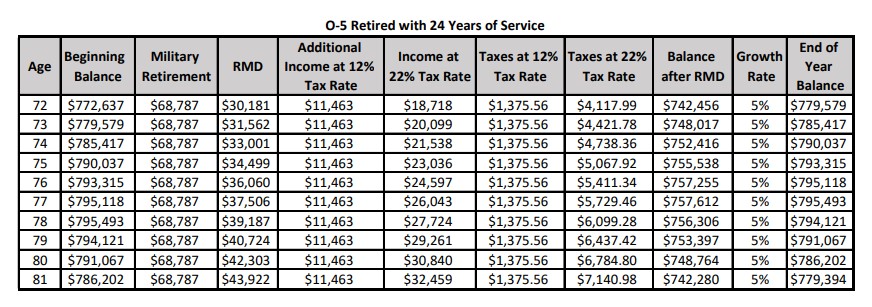

Example – O-5 Retiring at 24 Years of Military Service.

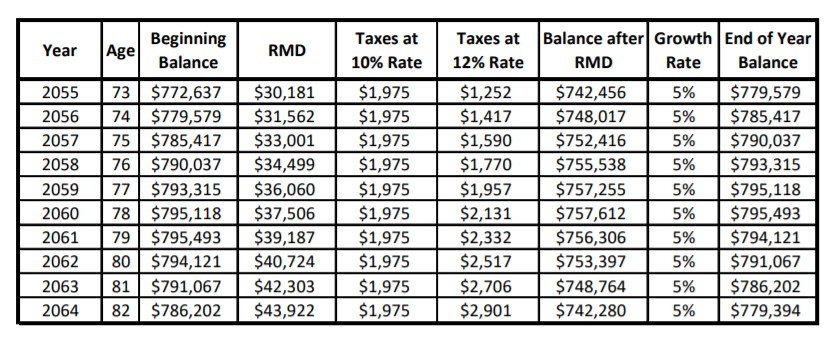

Going back to the estimated pay tables for an O-5, an O-5 retiring in 2021 with 24 years of service will retire with an estimated monthly pay of $5,732, or about $68,787 annually. Using the nest egg from my previous post of $772,637 with the same Required Minimum Distributions (RMDs) starting at age 72, you come up with the following results:

{kind=link}

{kind=link}

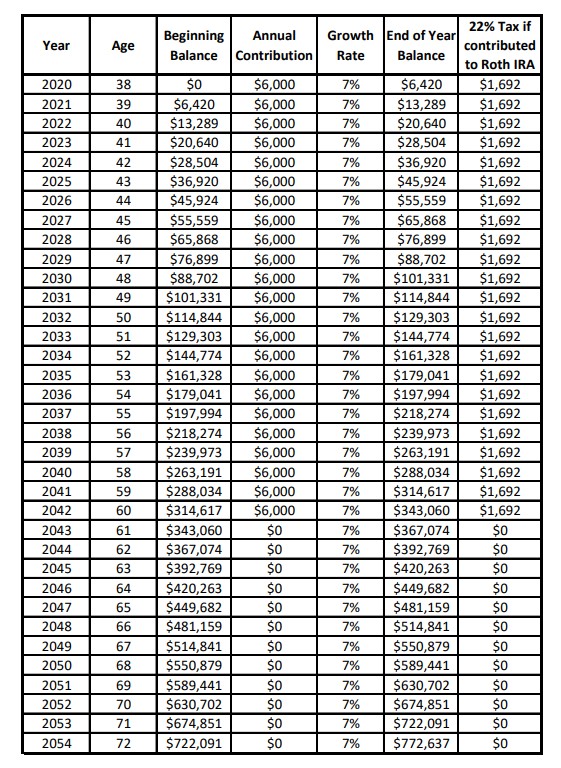

Recall that the nest egg was built with 23 contributions of $6,000 from 38 to 60 years old with a 7% growth rate. If you made those contributions in a Roth IRA or another Roth retirement account (Roth TSP, Roth 401(k), or any other), then you would have paid $38,923 in taxes when you were contributing. If you put those into traditional retirement accounts, you will pay a total of $69,705 in taxes during the first 10 years of RMDs. Those taxes don’t include any additional withdrawals before RMDs start happening or additional money withdrawn on top of RMDs after you turn 72 years old. If this retiree saves in a Roth retirement account instead of a traditional retirement account, they will pay $30,000 less in taxes during their first 10 years of RMDs.

{kind=link}

More Examples

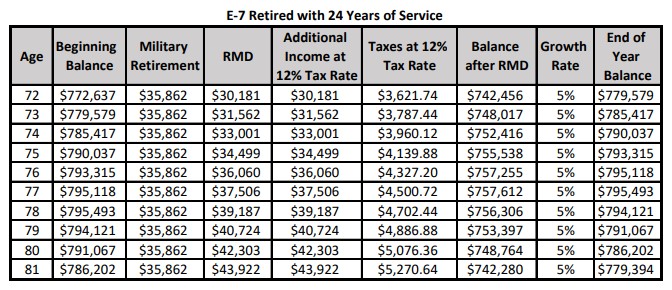

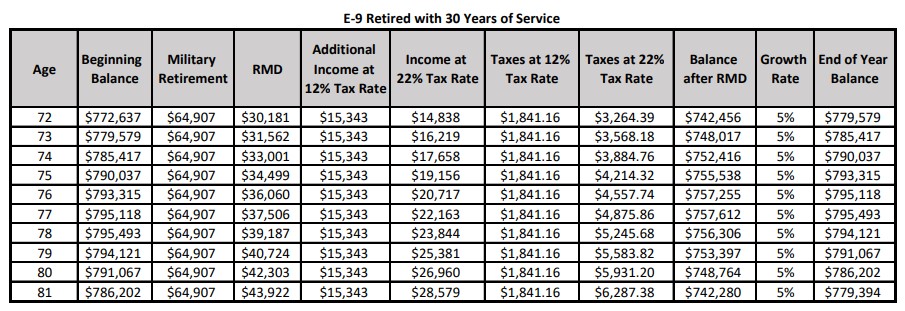

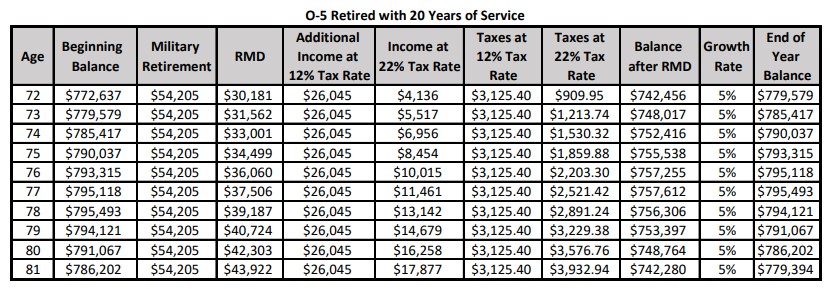

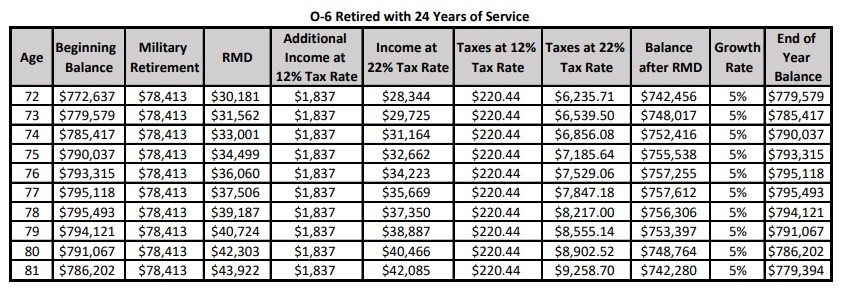

The table below shows a summary of various military retirements with the same nest egg and RMDs from ages 72 to 81. Keep in mind that taxes would be $38,923 for each of these potential military retirees if they contributed to Roth retirement accounts. The links in the table will bring up another table breaking down the RMD and taxes for each year as shown in the example above.

| Military Retirement (Rank & Years of service) | Beginning Balance | Military Retirement (annual amount) | 10 Years of RMDs | Total Taxes on RMDs | Continued Growth Rate | Balance after 10 Years of RMDs |

| E-6 w/ 22 Years | $772,637 | $27,055 | $368,945 | $44,273 | 5% | $779,394 |

| E-7 w/ 24 Years | $772,637 | $35,862 | $368,945 | $44,273 | 5% | $779,394 |

| E-8 w/ 26 Years | $772,637 | $45,070 | $368,945 | $47,136 | 5% | $779,394 |

| E-9 w/ 30 Years | $772,637 | $64,907 | $368,945 | $65,825 | 5% | $779,394 |

| O-5 w/ 20 Years | $772,637 | $54,205 | $368,945 | $55,123 | 5% | $779,394 |

| O-5 w/ 24 Years | $772,637 | $68,787 | $368,945 | $69,705 | 5% | $779,394 |

| O-6 w/ 24 Years | $772,637 | $78,413 | $368,945 | $79,331 | 5% | $779,394 |

| O-6 w/ 28 Years | $772,637 | $97,780 | $368,945 | $81,168 | 5% | $779,394 |

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

A Few Other Things to Think About

Even though these estimates assume a married couple filing jointly, remember taxes will only be higher for retirees that are single. None of these calculations include any social security income or a spouse’s retirement income, whether through a pension or retirement accounts. This also doesn’t include any other income from working, a business, or investments. For each of these additional types of income, you’ll pay more income in taxes and push closer to the next higher tax bracket.

Wrapping Up

Although the allure of having more money in your pocket today is very tempting, I hope you can see that you’ll end up with less in your pockets later (potentially a lot less) by using traditional retirement accounts instead of Roth accounts.

I tried to break down the numbers the best I could, so if you have any questions about the tables, let me know in a comment or send a comment in on the ‘Contact Us’ page.

In the next post, I’m going to continue with the retirement trend. I know some readers have been aggressively saving for retirement, so I’ll cover the tax implications of using traditional retirement accounts instead of Roth accounts with a much larger nest egg.

Sign Up for the Weekly Off Ramp! And send in a topic you want to hear about on the Contact Us page. Follow me on Twitter ![]() Facebook

Facebook ![]() and Pinterest

and Pinterest ![]()